Recommended Blogs

Blog

From AI Adoption to AI Accountability: What Insurers Need to Know in 2026

Table of Content

- Why 2026 is a Turning Point for Insurance AI Governance

- What Insurance AI Compliance Regulations in 2026 Are Really Asking For

- Where AI Creates the Highest Accountability Risk for Insurers

- The Insurance AI Governance Model Leaders Should Build Now

- How TxMinds Helps Insurers Move from AI Adoption to AI Accountability

Share On

AI is no longer a side experiment for insurers. It is beginning to shape underwriting judgment, claims handling, pricing discipline, fraud review, and customer interactions.

That creates a difficult leadership question. Can your organization scale AI while proving that every model, workflow, and automated decision remains fair, explainable, monitored, and controlled?

For C-level leaders in the insurance industry, 2026 should be treated as an accountability checkpoint. The companies that prepare early will not only reduce compliance exposure. They will also build stronger trust with regulators, customers, distribution partners, and internal teams.

This blog explains what insurance AI governance should mean in 2026. It also shows how leaders can prepare for insurance AI compliance regulations 2026 without slowing useful innovation.

Key Takeaways

- 2026 marks a shift from AI adoption to AI accountability for insurers using AI in underwriting, pricing, claims, fraud detection, and customer workflows.

- Insurance AI compliance regulations 2026 are pushing insurers to prove human oversight, explainability, vendor control, and continuous model monitoring.

- AI accountability risk is highest where models influence customer-impacting decisions, especially eligibility, pricing, claims outcomes, and fraud review.

- Strong insurance AI governance starts with practical controls, including AI inventory, risk classification, data trust, human review, and post-launch monitoring.

Why 2026 is a Turning Point for Insurance AI Governance

Insurance AI is moving from pilot programs into live business decisions. It now supports underwriting, pricing, claims triage, fraud review, and customer service workflows. That shift changes the leadership question. Insurers must now prove that AI-supported decisions are fair, monitored, explainable, and accountable.

The NAIC says its AI Model Bulletin sets expectations for responsible AI use by insurers, including governance, risk management, and accountability. That direction makes insurance AI governance a practical operating requirement, not just a compliance theme.

Accountability is becoming the real test

Efficiency was the first promise of insurance AI. Accountability is becoming the harder test for 2026. Leaders should be ready to answer five questions:

- Where is AI already used across the company?

- Which customer or business decisions does it influence?

- What data sources shape the model outputs?

- Who owns model performance and customer impact?

- How are bias, drift, and exceptions monitored?

The insurers that answer these questions early will move faster with less regulatory friction. The ones that delay may discover their AI risk only after scrutiny begins.

What Insurance AI Compliance Regulations in 2026 Are Really Asking For

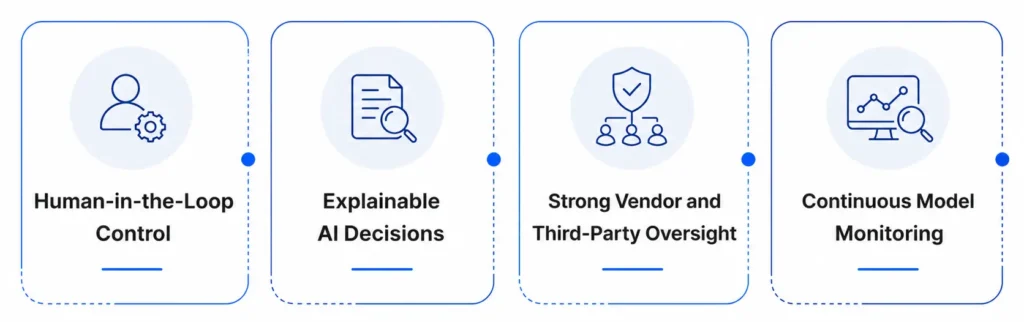

Insurance AI compliance regulations 2026 are asking insurers for one clear shift. AI must move from useful automation to accountable decision support. Regulators are not only looking at the technology itself. They are looking at whether insurers can prove oversight, fairness, explainability, monitoring, and vendor control.

-

Human-in-the-Loop Control

AI should not become the final authority for consequential insurance decisions. Human review must remain visible where decisions affect eligibility, pricing, claims, cancellations, or adverse outcomes. Teams should know when AI can recommend, when it can automate, and when a licensed or accountable human must step in.

-

Explainable AI Decisions

Black-box decisions are difficult to defend in regulated insurance workflows. Insurers need to understand why a model produced a recommendation, risk score, fraud flag, or pricing signal. Explainability should be built into the workflow, not added after deployment. Underwriters, claims leaders, compliance teams, and auditors need decision logic they can examine and challenge.

-

Strong Vendor and Third-Party Oversight

Using a third-party AI model does not remove the insurer’s responsibility. Vendor tools can still influence underwriting, claims, pricing, servicing, or fraud decisions. Insurers should review vendor data sources, model limitations, testing evidence, monitoring practices, and incident processes. The EU AI Act also reinforces a risk-based approach for AI systems, including obligations that can affect providers and deployers.

-

Continuous Model Monitoring

AI cannot be approved once and left alone. Models can drift when data changes, market behavior shifts, or business rules evolve. Insurers need ongoing monitoring for accuracy, bias, exception rates, overrides, and customer impact. Audit-ready records should show how the model performed after it entered real-world use.

Where AI Creates the Highest Accountability Risk for Insurers

Not every AI use case carries the same risk. A chatbot that summarizes internal policies is different from a model that affects eligibility or pricing. Leaders should classify AI use cases by business impact, customer consequence, data sensitivity, and regulatory exposure.

-

Underwriting and Pricing

Underwriting and pricing AI can improve speed, consistency, and risk selection. It also raises fairness concerns when models use external data, inferred attributes, or proxy signals.

Leaders need clear explainability, documented testing, and human review for decisions that affect eligibility, pricing, or coverage.

-

Claims and Fraud Detection

Claims AI can improve routing, document review, severity scoring, and fraud detection. The risk appears when automation delays, escalates, or influences claim outcomes without enough oversight.

Fraud models also need careful monitoring because false positives can damage trust and increase complaint risk.

-

Customer Data and Third-Party Models

Insurers often rely on external data, vendor models, and third-party AI platforms. That creates accountability risk even when the insurer did not build the model.

Vendor governance should cover data sources, model limits, testing evidence, monitoring rights, and incident processes.

The Insurance AI Governance Model Leaders Should Build Now

A strong governance model should help insurers scale AI with control. It should not slow innovation through unclear committees or heavy approval layers. The goal is practical discipline. Leaders need a model that separates low-risk experimentation from AI that affects customers, pricing, claims, eligibility, or regulated decisions.

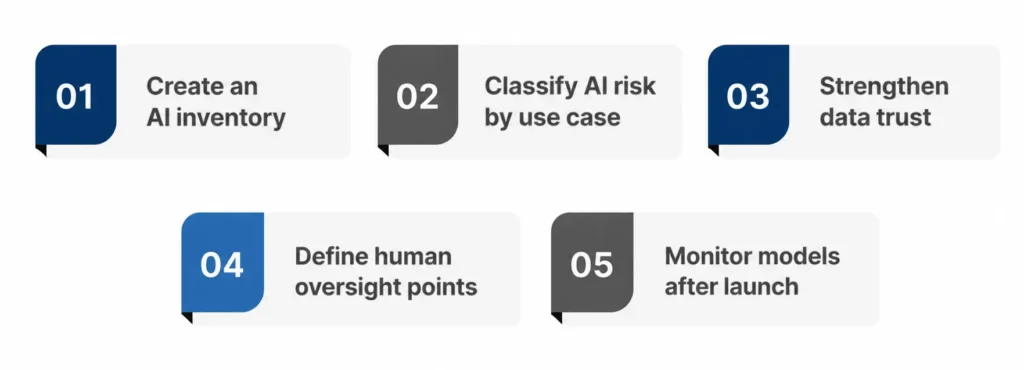

To build stronger insurance AI governance, insurers should focus on these core actions:

- Create an AI inventory: Track where AI is used, who owns it, what decisions it supports, and which data sources it uses.

- Classify AI risk by use case: Separate low-risk productivity tools from high-risk systems that influence customer or regulatory outcomes.

- Strengthen data trust: Confirm data lineage, quality, access controls, retention rules, and consent alignment before models scale.

- Define human oversight points: Decide when AI can recommend, when it can automate, and when human approval is mandatory.

- Monitor models after launch: Track accuracy, bias, drift, exceptions, overrides, complaints, and vendor performance continuously.

Insurance AI governance works best when it becomes part of daily operations. The strongest insurers will not wait for audits to reveal AI gaps. They will build control into the way AI is designed, deployed, monitored, and improved.

How TxMinds Helps Insurers Move from AI Adoption to AI Accountability

At TxMinds, we help insurers move from AI experimentation to governed, scalable execution. We work with leaders who need AI systems that support growth, compliance, trust, and operating control.

We approach insurance AI governance as an enterprise technology challenge. That means connecting AI engineering, data trust, platform modernization, quality assurance, cybersecurity, and domain workflows. We help insurers assess AI readiness, map high-risk use cases, strengthen data foundations, and design governance-ready delivery models. We also support modernization across underwriting, claims, policy systems, integrations, and managed operations.

For insurers preparing for insurance AI compliance regulations 2026, TxMinds brings domain-aware engineering and responsible AI delivery together. To strengthen AI accountability without slowing innovation, connect with TxMinds.

Associate Director

Yuvraj Singh is an accomplished Associate Director of Delivery, renowned for leading strategic quality assurance initiatives that consistently deliver outstanding software outcomes across global markets. With deep expertise in both Property & Casualty (P&C) and Life & Annuities (L&A) insurance domains, Yuvraj excels at bridging the gap between complex business objectives and flawless execution.

FAQs

What is insurance AI governance?

Insurance AI governance is the set of controls insurers use to manage AI responsibly across underwriting, pricing, claims, fraud detection, servicing, and operations. It covers AI ownership, data quality, explainability, human oversight, monitoring, vendor control, and audit readiness.

Why does insurance AI governance matter in 2026?

Insurance AI governance matters in 2026 because AI is moving into customer-impacting decisions. Insurers must show that AI-supported workflows are fair, explainable, monitored, and accountable before regulatory scrutiny or customer complaints expose control gaps.

What should insurers know about insurance AI compliance regulations 2026?

Insurance AI compliance regulations 2026 are pushing insurers toward stronger documentation, bias monitoring, human review, model validation, and third-party oversight. Leaders should treat compliance as an operating discipline, not a one-time legal checklist.

Which insurance AI use cases need the strongest governance?

The strongest governance is needed where AI influences eligibility, pricing, underwriting decisions, claims outcomes, fraud review, cancellations, or adverse customer actions. These use cases carry higher accountability risk because they can directly affect policyholders.

Discover more