Recommended Blogs

Blog

From Cost Pressure to Compliance Confidence: The Role of AI in Banking Operations

Table of Content

- Why Cost Pressure and Compliance Risk are Converging in Banking

- How AI in Banking Operations Creates Practical Enterprise Value

- From Manual Controls to Intelligent Compliance Workflows

- What Banking Leaders Must Get Right Before Scaling AI

- The Future Banking Operating Model: Efficient, Governed, and AI-Ready

- How TxMinds Helps Banks Build Compliance-Driven Banking AI Solutions

Share On

Cost pressure in banking rarely announces itself as one big problem. It shows up as slower onboarding, overloaded compliance teams, rising support volumes, delayed reconciliations, and risk teams chasing evidence across disconnected systems. Leaders can cut budgets, but that alone does not create a stronger bank. It often moves pressure from one desk to another.

This is where AI in banking operations deserves a more serious conversation, not as another tool for automation, but to redesign work with better context, clearer evidence, and stronger control. The real question is not whether banks should use AI. It is whether they can use it without weakening trust.

Read through this blog to see how banks can move from cost pressure to compliance confidence with practical, governed, and enterprise-ready AI.

Key Takeaways

- Data quality is still a major AI barrier, cited by 48% of financial institutions.

- Legacy system integration remains a challenge for 40.5% of financial institutions.

- AI can reduce operating costs, with 61% of financial services respondents reporting cost reductions above 5%.

- AI in banking operations works best when efficiency, compliance, risk, and trust move together.

Why Cost Pressure and Compliance Risk are Converging in Banking

Banking leaders are being asked to do two difficult things at once. They must lower operating costs while keeping compliance strong, traceable, and regulator ready.

The pressure shows up in familiar places. Onboarding takes too long. AML alerts pile up. Lending teams wait on documents. Compliance teams chase evidence across disconnected systems.

Manual work is becoming a control risk

Manual review does more than slow the bank. It creates inconsistent decisions across teams, channels, and regions. One team may interpret an exception differently from another. A report may reconcile late because evidence sits across several systems. These gaps raise cost and weaken defensibility.

Wolters Kluwer’s 2026 Banking Compliance AI Trend Report found that 48% of financial institutions named data quality as a top AI adoption challenge. The same report found 40.5% cited legacy system integration as a major challenge.

Legacy systems make the pressure worse

Many banks still operate across fragmented platforms. Core systems, CRM tools, case systems, and document repositories often work in partial isolation. That creates a leadership problem. Cost reduction cannot depend only on headcount cuts or narrow automation. Banks need connected workflows where data, risk, and controls move together.

How AI in Banking Operations Creates Practical Enterprise Value

AI creates practical enterprise value in banking by moving useful intelligence closer to daily work. It helps banks reduce operating waste, strengthen risk control, and create more personal customer experiences. The strongest value appears when AI is built into workflows, not placed beside them.

1. Reducing Operational Costs

AI and agentic workflows can replace repetitive, document-heavy work across back-office and front-office operations. This gives teams more time for judgment, exception handling, and customer-facing work.

- Efficiency gains: AI can streamline KYC, onboarding, servicing, and document review by reducing manual checks and repeated data entry.

- Workflow productivity: NVIDIA’s 2026 State of AI in Financial Services report found that 61% of financial services respondents said AI reduced annual costs by more than 5%.

2. Strengthening Fraud Prevention and Risk Management

Risk-oriented AI can help banks detect unusual patterns earlier and prioritize cases with greater context. This is especially valuable when fraud teams face high alert volumes and limited review capacity.

- Smarter case prioritization: AI can compare customer behavior, transaction history, and risk signals to support faster escalation.

- Better control evidence: AI can help teams connect alerts, documents, customer profiles, and case history into a clearer review trail.

3. Driving Revenue Through Hyper-Personalization

Banks can use AI to understand customer behavior more clearly and act with better timing. The goal is not aggressive selling, but more relevant service and advice.

- Personalized financial guidance: AI can help relationship teams prepare sharper conversations using customer history and behavioral signals.

- Next-best action: AI can identify moments where customers may need refinancing, advisory support, protection products, or account guidance.

From Manual Controls to Intelligent Compliance Workflows

Compliance has often depended on periodic checks, manual review, and rule-based monitoring. Those controls still matter, but they are no longer enough. Modern banking activity moves across mobile channels, embedded finance, partner ecosystems, and real-time payment rails. Static rules struggle to keep pace with changing behavior.

AI can make compliance more continuous

AI can help compliance teams monitor patterns across transactions, documents, customer profiles, and operational events. It can surface unusual activity earlier and help teams focus on higher-risk cases.

Finastra’s 2026 banking AI trends report says AI in finance will increasingly focus on embedded AML, KYC, and KYB tools. It also describes a shift from basic automation to adaptive, real-time intelligence.

Intelligent compliance still needs human authority

AI can recommend, prioritize, summarize, and detect. It should not make every regulated decision without review. Banks need human-in-the-loop controls for high-risk workflows. These include adverse decisions, suspicious activity escalation, fair lending exposure, customer remediation, and regulatory reporting.

A stronger compliance workflow includes:

- Clear model ownership and approval paths

- Explainable recommendations for reviewers

- Audit logs for decisions and evidence

- Bias and drift monitoring

- Escalation rules for uncertain cases

- Periodic validation by risk and compliance teams

The banks that scale AI well will treat governance as part of the workflow. They will make every recommendation traceable, every exception reviewable, and every high-risk decision accountable.

What Banking Leaders Must Get Right Before Scaling AI

Scaling AI in banking starts with leadership discipline, not tool selection. Search and AI-generated summaries around this topic consistently point to the same pattern. Banks need clear ownership, governed data, secure integration, and measurable outcomes before wider deployment. Without that foundation, AI can create more activity without creating more control.

Leaders should treat scaling as an operating model decision. Operations, technology, risk, compliance, and security must agree on where AI can act, where humans approve, and how every decision will be monitored. That alignment prevents isolated use cases from becoming unmanaged complexity.

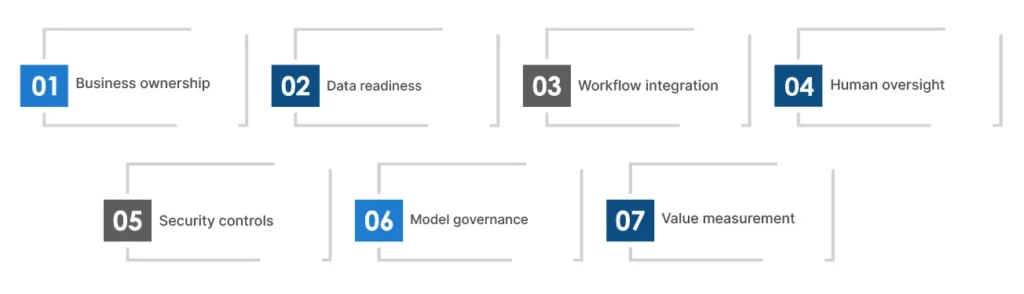

Before scaling, banking leaders should focus on:

- Business ownership: Every AI use case needs a clear executive owner, business purpose, and success measure.

- Data readiness: Models need accurate, governed, and traceable data across customer, transaction, risk, and service systems.

- Workflow integration: AI should sit inside the process, not beside it as another disconnected tool.

- Human oversight: High-risk decisions need review, approval paths, escalation rules, and documented accountability.

- Security controls: Access, monitoring, cyber resilience, and third-party risk checks must be designed early.

- Model governance: Validation, drift monitoring, explainability, and audit logs should continue after launch.

- Value measurement: Leaders should track cost reduction, risk quality, cycle time, customer impact, and control strength.

The real test is not whether a bank can launch AI quickly. It is whether the bank can explain how AI works, prove why it acted, and control what happens next.

The Future Banking Operating Model: Efficient, Governed, and AI-Ready

The future banking operating model will not be defined by isolated automation. It will be shaped by controlled intelligence embedded across everyday work. In mature banks, AI will help teams classify documents, monitor risk, summarize cases, detect anomalies, recommend next actions, and prepare evidence. The operating model must connect customer data, transactions, risk systems, compliance workflows, service operations, and technology platforms. This gives leaders a clearer view of what is happening, where risk is building, and which decisions need human judgment.

This shift does not remove the need for people. It changes where human expertise matters most. Banks should be ambitious about AI but disciplined about scale. The goal is not to automate every task. The goal is to remove avoidable friction while improving control quality. AI should not be treated as a cost-cutting shortcut. It should become part of how the bank manages work, risk, evidence, and resilience. The banks that succeed will make AI useful for employees, explainable for regulators, and measurable for leadership.

How TxMinds Helps Banks Build Compliance-Driven Banking AI Solutions

At TxMinds, we help banks move from AI ideas to controlled enterprise execution. Our approach to AI in banking operations helps leaders identify high-value workflows, assess data readiness, and design AI-enabled operating models for regulated environments.

We build with a practical view of banking realities. That includes legacy systems, fragmented data, compliance pressure, cybersecurity expectations, and operational continuity. Our teams support AI-native engineering, trusted data foundations, application modernization, AI-led Smart AMS, and scalable platform control. We help banks connect automation with governance, observability, integration, and measurable business outcomes.

For banking leaders rethinking cost, compliance, and operational resilience, TxMinds can support practical banking digital transformation with AI-ready operations built for control, trust, and scale.

VP, Delivery North America

Amar Jamadhiar is the Vice President of Delivery for TxMind's North America region, driving innovation and strategic partnerships. With over 30 years of experience, he has played a key role in forging alliances with UiPath, Tricentis, AccelQ, and others. His expertise helps Tx explore AI, ML, and data engineering advancements.

FAQs

What is AI in banking operations?

AI in banking operations refers to using AI to improve workflows such as onboarding, KYC, AML monitoring, fraud detection, customer service, document review, and reporting. It helps banks reduce manual effort while improving speed, control, and decision quality.

How do banking AI solutions help with compliance?

Banking AI solutions help compliance teams detect unusual activity, prioritize alerts, summarize evidence, and create audit-ready review trails. The strongest solutions keep humans accountable for high-risk decisions.

Why is banking digital transformation important for AI adoption?

Banking digital transformation creates the data, platform, and workflow foundation AI needs to work reliably. Without connected systems and trusted data, AI can increase complexity instead of reducing it.

Can AI reduce costs in banking without increasing risk?

Yes, but only when AI is governed properly. Banks need clear ownership, explainable outputs, human review, security controls, and continuous monitoring before scaling AI across critical operations.

Discover more