Recommended Blogs

Blog

How Leading Banks Modernize Data Infrastructure Without Pausing Operations

Table of Content

- Why Banking Data Infrastructure is Under Pressure

- Why Big-Bang Modernization Creates Operational Risk

- The Modernization Roadmap Leading Banks Follow

- The Control Layer: Governance, Observability, and Trust

- Building AI-Ready and Cloud-Ready Banking Data Platforms

- How TxMinds Helps Banks Modernize Data Infrastructure with Control

Share On

Banks do not get quiet weekends for transformation anymore. Payments still clear, credit decisions still move, fraud teams still monitor risk, and regulators still expect accurate reporting. Yet the data foundations behind these functions are often stretched beyond their original design.

That is why banking data modernization has become a leadership priority, not a back-office technology project. Banks need cleaner data flows, stronger governance, faster access, and infrastructure that can support AI, real-time decisions, and regulatory confidence.

For CIOs, CTOs, and CDOs, the value is practical. Modernizing banking data infrastructure can improve resilience, reduce operational friction, and prepare the bank for AI-enabled growth. The challenge is doing it without disrupting operations that customers, regulators, and business teams expect to run continuously.

Key Takeaways

- Banking data modernization must protect always-on operations across payments, lending, risk, compliance, and customer channels.

- Big-bang migration creates avoidable risk, so leading banks modernize through phased rollout, coexistence, validation, and rollback readiness.

- Governance and observability help banks protect data trust by improving lineage, ownership, quality control, access visibility, and issue detection.

- AI-ready banking depends on trusted, governed, and scalable data infrastructure that can support real-time decisions and enterprise growth.

Why Banking Data Infrastructure is Under Pressure

Banking data infrastructure now carries more responsibility than traditional reporting workloads. It supports fraud alerts, personalization, credit risk, liquidity insight, compliance, payments intelligence, and AI-enabled workflows.

Many banks still depend on batch-heavy pipelines and tightly coupled legacy platforms. These systems often work well enough to survive, but not well enough to scale. The pressure appears when business teams need faster data, cleaner lineage, and better confidence.

AI has raised the data standard

AI in banking does not fail only because models underperform. It fails when data is incomplete, poorly governed, delayed, or hard to explain. BCG’s 2026 view of the bank CIO argues that CIOs must now connect AI, data, and strategy amid rising complexity and regulation.

That shift changes the modernization question. Leaders are not simply asking whether the warehouse should move. They are asking whether the bank can trust its data foundation under pressure.

Operational expectations have changed

Modern banking runs on real-time expectations. Customers expect instant balances, fast approvals, contextual offers, and timely fraud protection. Regulators expect traceability and control.

That means data modernization in banking must serve two outcomes together.

- Faster access to trusted data

- Stronger control over how data moves

The tension is real. Moving faster can increase risk when governance is weak. Adding controls can slow teams when architecture is outdated.

Why Big-Bang Modernization Creates Operational Risk

A bank cannot treat data modernization like a simple platform swap. The data estate usually touches payments, lending, treasury, compliance, finance, risk, CRM, and customer channels.

One hidden dependency can break reporting. One mapping error can weaken reconciliation. One late cutover issue can affect a customer-facing process.

The risk is not only downtime

Downtime is visible, but trust damage can be worse. A bank can keep systems online and still lose confidence if reports stop reconciling. Business users may then return to spreadsheets, local extracts, and shadow processes. That is how modernization quietly fails. The new platform exists, but adoption stalls.

A 2026 practitioner paper on regulated-enterprise reconciliation notes that banks often operate across heterogeneous systems that were not designed to interoperate. It highlights reconciliation, semantic standardization, anomaly detection, and governance as essential architecture patterns.

Big-bang programs create late surprises

Large one-time migrations often push complexity toward the end. Teams discover data quality gaps during testing. Business users find report differences near cutover. Security teams uncover access issues after migration design is already fixed.

A safer approach usually includes:

- Parallel operation between legacy and modern platforms

- Continuous reconciliation across critical data flows

- Business validation before decommissioning legacy logic

- Rollback readiness for high-risk workloads

- Observability across pipelines, APIs, and downstream reports

This is how banks modernize data infrastructure without downtime. They prove trust before they force change.

The Modernization Roadmap Leading Banks Follow

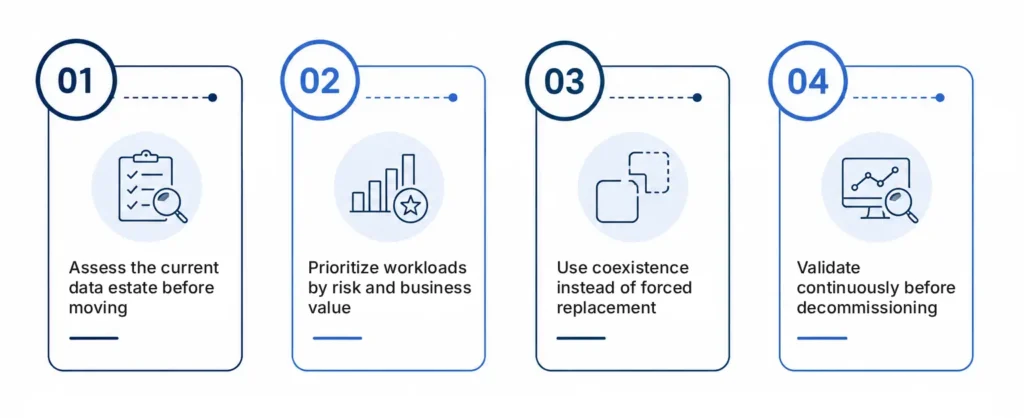

A practical banking data modernization roadmap for CIOs starts with sequencing. Every workload does not deserve the same urgency, risk treatment, or migration path. The strongest programs begin with clarity before architecture decisions. Leaders identify what the bank must protect, improve, and enable.

-

Assess the current data estate before moving

A data estate assessment should go beyond a system inventory. It should explain how data actually moves through the bank. Teams should map:

- Critical data domains and owners

- Source systems and downstream consumers

- Data quality issues and reconciliation gaps

- Regulatory reporting dependencies

- Batch windows, latency, and performance limits

- Security, retention, and access patterns

This work may feel slow at first. It usually saves time later. Banks that skip discovery often pay through rework, delayed cutovers, and weaker adoption.

-

Prioritize workloads by risk and business value

Not every workload should move first. A low-risk analytics sandbox may help test patterns, but it may not reveal real banking complexity. Better pilots use meaningful workloads with controlled exposure. Fraud analytics, customer 360, regulatory reporting support, and credit decision data can reveal integration needs early.

The decision should consider three questions:

- Which workloads create visible business value?

- Which workloads expose modernization risks safely?

- Which workloads build reusable architecture patterns?

This creates a data infrastructure modernization strategy for banks that can scale.

-

Use coexistence instead of forced replacement

Coexistence is often the practical middle path. Legacy systems continue serving critical functions while modern platforms take on selected workloads. This model can use replication, APIs, event streams, data virtualization, and governed data products. The goal is not permanent duplication. The goal is controlled transition.

Still, banks should avoid replacing deep domain logic blindly. Some legacy logic contains years of regulatory and operational learning. It must be understood before it is retired.

-

Validate continuously before decommissioning

Validation should not wait for the final migration window. It should run throughout modernization. Strong validation covers:

- Record counts and reconciliation

- Transformation logic and business rules

- Performance under peak workloads

- Access controls and audit trails

- Report matching and user acceptance

- Data lineage across source and serving layers

Decommissioning should happen only after trust is proven. Otherwise, the bank may remove the very system that explains the numbers.

The Control Layer: Governance, Observability, and Trust

Banking data governance cannot be bolted on after migration. By then, data products, access models, and operational behaviors are already forming. Governance must sit inside the modernization design. It should define who owns data, how quality is measured, where lineage is visible, and who can approve changes.

Governance must become operational

Static policy documents do not control modern data flows. Banks need governance that operates inside pipelines, platforms, and workflows. That means metadata, classification, role-based access, retention rules, quality checks, and audit evidence should travel with the data. This keeps modernization useful without making control manual.

Observability protects always-on operations

Data observability gives leaders early warning when pipelines slow, fail, drift, or produce unusual outputs. It helps teams see quality issues before business users lose confidence.

For banks, observability should cover latency, freshness, completeness, schema changes, anomaly detection, and usage patterns. It should also connect technical incidents with business impact.

This is especially important for real-time data infrastructure in banking. Fraud, payments, digital onboarding, and risk monitoring all depend on timely data.

Building AI-Ready and Cloud-Ready Banking Data Platforms

AI-ready data infrastructure for banks is not only about storing more data. It is about making the right data trusted, governed, discoverable, and usable.

Cloud data modernization in banking can support that goal. It can improve scalability, analytics performance, integration flexibility, and experimentation speed. Yet cloud migration alone does not create trust.

Cloud should follow workload logic

Some workloads fit cloud-native platforms quickly. Others may require hybrid patterns because of latency, residency, cost, or regulatory constraints.

A practical cloud data modernization strategy should classify workloads by business criticality, sensitivity, performance needs, and integration complexity. This avoids moving data simply because a platform is available.

AI readiness depends on data discipline

AI needs curated, contextual, and governed data. It also needs human accountability, monitoring, and security controls. A modern banking data platform should support:

- Governed data products

- Real-time and batch processing

- Clear lineage and metadata

- Secure access across teams

- Integration with core banking systems

- Scalable analytics and AI workflows

How TxMinds Helps Banks Modernize Data Infrastructure with Control

At TxMinds, we help banks modernize data infrastructure without treating continuity as an afterthought. We work with leaders to assess current data estates, identify critical dependencies, and shape phased modernization roadmaps.

We bring data engineering, cloud modernization, platform scalability, AI-native engineering, and governance thinking into one delivery approach. Our teams help design coexistence models, migration paths, validation routines, observability layers, and trusted data pipelines.

We also focus on the operating model behind the technology. That includes ownership, data quality controls, business acceptance, and readiness for AI-enabled banking use cases.

For banking leaders, our goal is straightforward. We help modernize data foundations while protecting trust, compliance, and day-to-day operations. If your bank is rethinking data modernization, TxMinds can help shape a controlled, AI-ready path forward.

VP and Global Head Data & AI Practice

Results-oriented Data Analytics & AI Specialist with 24+ years of experience in multiple roles, including Practice Leader with P&L ownership. Expert in building Data Analytics practices, defining market strategies, and leading large-scale transformation initiatives. Skilled in Business Intelligence, Data Engineering, Cloud platforms (Azure, AWS, GCP), AI/ML, and Data Governance, with a strong focus on customer-centric solutions and strategic alliances.

Discover more