Recommended Blogs

Blog

Insurance Modernization: Why Legacy Core Systems are Becoming a Growth Constraint

Table of Content

- Key Takeaways

- The Hidden Growth Tax of Standing Still in Insurance

- Why Legacy Core Systems are Silently Limiting the Next Era of Insurance Growth

- Insurance Digital Transformation Begins Where the Enterprise Truly Runs: The Core

- From Operational Risk to Enterprise Resilience: The Imperative for Insurance Core System Modernization

- Cloud in the Insurance Data Modernization Industry: The Multiplier for Speed, Intelligence, and Scale

- How TxMinds Accelerates Insurance Digital Transformation with Confidence and Control

Share On

For years, legacy core systems gave insurers stability, control, and operational confidence. Now, the same systems are quietly deciding how fast the business can grow. New products wait for configuration cycles. Claims journeys depend on manual recovery. Data sits across systems that were never built to think together.

This is where the real modernization question begins. Can an insurer lead the next market cycle with a core built for the last one?

The opportunity is no longer limited to cost reduction. McKinsey’s 2026 insurance analysis found that agentic AI can deliver typical productivity improvements of 10 to 90 percent across core modernization activities, including testing, reconciliation, data mapping, and governance. For C-level leaders, that changes the conversation. Insurance digital transformation becomes a route to speed, resilience, intelligence, and strategic freedom.

Read this blog to explore why legacy core systems are becoming a growth constraint, and how insurance data management services can turn the core into a competitive advantage.

Key Takeaways

- Legacy core systems are no longer just IT challenges. They are becoming growth constraints that slow product launches, claims, personalization, and ecosystem expansion.

- Insurance digital transformation must start at the core. Without modern policy, billing, claims, and data foundations, front-end innovation remains limited.

- McKinsey’s 2026 insurance analysis found that agentic AI can deliver productivity improvements of 10 to 90 percent across core modernization activities.

- Cloud migration in the insurance industry works best when tied to modernization goals. It helps insurers improve speed, intelligence, scalability, and resilience.

The Hidden Growth Tax of Standing Still in Insurance

Legacy core systems rarely fail loudly. They work, until growth depends on them moving faster. That is why they are so dangerous. They create drag across pricing, products, claims, distribution, compliance, and customer experience. The enterprise still functions, but every strategic move takes longer than it should.

The cost is not only technical

A legacy platform can look stable on a dashboard. Yet the business feels its limitations every day. A new product may need months of configuration. A pricing change may require manual workarounds. A claims enhancement may depend on brittle integrations. A digital channel may need duplicate data entry behind the scenes.

Where growth starts to slow

For large insurers, standing still creates four visible consequences.

- Product innovation becomes harder to scale.

- Data remains fragmented across critical functions.

- Customer journeys depend on manual recovery.

- Transformation budgets fund maintenance instead of advantage.

McKinsey notes that P&C core systems built for slower, paper-driven models are no longer fit for purpose. They leave carriers facing inefficiency, rising IT maintenance costs, and pressure for real-time responsiveness.

Why Legacy Core Systems are Silently Limiting the Next Era of Insurance Growth

Legacy core systems are not failing because they are old. They are failing because the business around them has changed. Insurers now need speed, embedded partnerships, real-time data, and personalized experiences. Many core platforms were never designed for that kind of operating model.

The result is a quiet constraint on growth. The enterprise can still function, but it cannot always move with conviction.

1. Inability to Support Real-Time and Embedded Ecosystems

Modern insurance growth increasingly depends on instant decisions and connected ecosystems. Legacy systems often depend on batch processing, rigid workflows, and delayed data movement.

That creates friction where speed matters most. Underwriting decisions slow down. Partner integrations take longer. Embedded insurance opportunities become harder to launch and scale.

2. Poor Customer Experience and Limited Personalization

Customers may see a digital front end. Behind it, teams may still work through fragmented records, duplicate processes, and manual interventions.

This gap weakens personalization. It also makes service inconsistent across policy, billing, claims, and support touchpoints. A modern customer journey needs a unified view of the customer. Legacy cores often make that view difficult to create and harder to trust.

3. Data Analytics and AI Bottlenecks

Insurance digital transformation depends on data that is accessible, governed, and usable. Legacy systems often trap data inside isolated platforms and aging data models.

That limits analytics, automation, and AI adoption. Claims intelligence, predictive underwriting, fraud detection, and real-time reporting all depend on clean data flows. Without a modern core, AI becomes difficult to scale beyond pilots.

4. Financial and Operational Drag

Legacy systems consume attention long after they stop creating advantage. They require specialized skills, custom fixes, and constant maintenance.

Security also becomes harder to manage when platforms cannot support modern controls. Every workaround adds more complexity to an already fragile environment.

Insurance Digital Transformation Begins Where the Enterprise Truly Runs: The Core

Insurance digital transformation is often misunderstood. It is not a portal strategy, an app launch, or a collection of automation projects. Those may be visible outcomes, but the real transformation happens deeper. It happens when the core enterprise can sense, decide, and act faster through modern architecture, connected data, governed automation, and resilient delivery.

The core determines the transformation ceiling

If core systems remain rigid, digital transformation hits a ceiling quickly. Teams may improve individual journeys, but enterprise-wide speed remains out of reach. Underwriting waits for data, claims depend on disconnected evidence, and service teams still navigate fragmented systems.

A modernized core changes that equation. It gives the enterprise a cleaner operating spine for real-time data movement, API-led integration, automated workflows, and faster product configuration.

Insurance core system modernization must protect continuity

Executives are right to be cautious. Insurance core system modernization touches revenue, compliance, service, and trust. A reckless transformation can disrupt the business, while a passive strategy can weaken it slowly.

The wiser path is deliberate modernization, built around phased migration, strong governance, and business-aligned quality engineering. Deloitte’s 2026 insurance outlook says legacy system modernization remains a top focus for insurers, with many pursuing multi-year, cloud-based transformations while balancing near-term needs with future AI models.

From Operational Risk to Enterprise Resilience: The Imperative for Insurance Core System Modernization

Insurance core system modernization is an enterprise resilience decision. A modern core improves how the business absorbs change. It helps insurers respond to market shifts, regulatory demands, catastrophe events, partner expansion, and customer expectations.

Resilience is built through design

Modernization should simplify what the enterprise runs. It should reduce avoidable customization. It should create cleaner data flows and stronger controls.

The most effective programs usually focus on five priorities.

1. Business capability mapping

Leaders identify which capabilities drive differentiation and which create operational drag.

2. Product and rules rationalization

Teams decide what must be preserved, redesigned, retired, or standardized.

3. Data readiness and governance

Migration planning starts with data meaning, lineage, quality, and reconciliation.

4. Integration modernization

APIs and event-driven patterns replace brittle point-to-point dependencies.

5. Quality engineering from day one

Testing, compliance, performance, and security become continuous disciplines.

This is where many programs succeed or stall. The largest modernization risks often emerge late, especially in data conversion, regression testing, reconciliation, and cutover readiness.

Cloud in the Insurance Data Modernization Industry: The Multiplier for Speed, Intelligence, and Scale

Cloud migration in the insurance industry is no longer a narrow IT upgrade. It has become a strategic shift in how insurers build, launch, analyze, and scale. When insurers move beyond rigid infrastructure and legacy hosting models, they create a foundation for faster innovation, stronger resilience, and more intelligent decision-making.

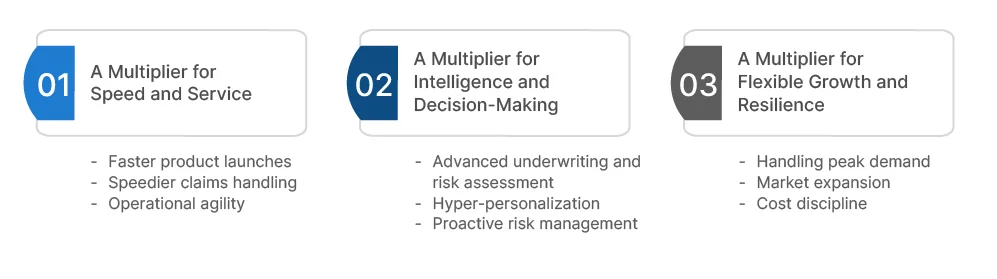

1. A Multiplier for Speed and Service

Cloud gives insurers the flexibility to build and release new capabilities with greater confidence. It reduces dependency on slow provisioning cycles and fixed infrastructure constraints.

- Faster product launches: Teams can test, configure, and deploy new products with fewer infrastructure delays.

- Speedier claims handling: Automation and connected workflows can help claims teams act faster.

- Operational agility: API-led and cloud-native models reduce reliance on manual IT processes.

2. A Multiplier for Intelligence and Decision-Making

Cloud enables insurers to connect data across systems and apply analytics at enterprise scale. This matters because smarter decisions depend on data that moves freely and securely.

- Advanced underwriting and risk assessment: Teams can use richer data signals to refine pricing and risk selection.

- Hyper-personalization: Cloud analytics can support more relevant customer journeys and service experiences.

- Proactive risk management: Better data access helps insurers anticipate risk instead of only reacting to it.

3. A Multiplier for Flexible Growth and Resilience

Insurance demand is rarely static. Renewal cycles, catastrophe events, market expansion, and partner growth can all create sudden pressure.

- Handling peak demand: Cloud environments can support high-volume periods without slowing critical services.

- Market expansion: Insurers can extend digital services and partner integrations across regions more easily.

- Cost discipline: Flexible consumption models help shift spending toward business value, not idle capacity.

For insurers, cloud migration is not about moving infrastructure somewhere else. It is about creating a business environment where speed, intelligence, and resilience can work together. The real value comes when cloud becomes part of the modernization roadmap, not a standalone technology project.

How TxMinds Accelerates Insurance Digital Transformation with Confidence and Control

At TxMinds, we help insurers modernize core operations with AI-enabled automation, platform-led modernization, and compliance-ready delivery. Our insurance data management services focus on outcomes that matter to leadership, including faster decisions, lower leakage, stronger governance, and audit-ready execution at scale.

We support modernization across claims, underwriting, quality engineering, legacy systems, ecosystem support, and cloud migration. Our teams design AI-led claims automation, risk analytics, and decision support while keeping governance, traceability, and compliance at the center.

Our approach is structured from solution design to implementation, testing, compliance validation, and ongoing optimization. We help insurers move forward with speed, resilience, and control, without putting critical operations at unnecessary risk.

Yuvraj Singh

Associate Director

Yuvraj Singh is an accomplished Associate Director of Delivery, renowned for leading strategic quality assurance initiatives that consistently deliver outstanding software outcomes across global markets. With deep expertise in both Property & Casualty (P&C) and Life & Annuities (L&A) insurance domains, Yuvraj excels at bridging the gap between complex business objectives and flawless execution.

FAQs

What is insurance digital transformation?

Insurance digital transformation is the modernization of core systems, data, workflows, and customer journeys to help insurers operate faster, smarter, and more resiliently. It goes beyond digital portals and focuses on how the enterprise actually runs.

Why is insurance core system modernization important?

Insurance core system modernization helps insurers reduce technical debt, improve data flow, accelerate product launches, and support better claims and underwriting decisions. It also gives leaders more control over transformation risk.

How does cloud migration help the insurance industry?

Cloud migration in the insurance industry helps insurers improve scalability, agility, analytics, and resilience. It supports faster deployment, better ecosystem integration, and stronger foundations for AI-led innovation.

When should insurers modernize legacy core systems?

Insurers should consider modernization when legacy systems slow product changes, limit personalization, increase maintenance effort, or block real-time data access. These signs often indicate that the core has become a growth constraint.

Discover more