Insurance has always been a data business, but the economics of the industry are changing faster than the carrier’s capabilities. Aspects such as pricing adequacy, fraud, customer retention, and loss-cost volatility now depend on the enterprise’s ability to integrate policy, claims, billing, and third-party data and turn it into informed decisions.

Yet, many insurers rely on fragmented core systems and analytics that sit outside day-to-day underwriting and claims. The result is a paradox. Though carriers are capturing more data than ever, they cannot convert it into advantages.

This blog explores the surge in demand for data analytics in insurance. We’ll also look at why traditional insurers often fail to realize its value and where to start making data a repeatable advantage.

Key Takeaways

Insurance analytics are projected to reach USD 54.47B by 2033, driven by fraud, complex claims, and personalization.

Legacy, siloed systems, and poor data quality stop insurers from getting a single, trusted customer/risk view.

Insurers should focus on 3–5 high-value data use cases, then fix data, unify systems, and scale AI.

Leaders like Allstate and MetLife use AI/ML to cut FNOL time, boost fraud detection, improve pricing, and lift retention.

The Growing Demand for Data Analysis in Insurance Organizations

The insurance analytics market size is projected to reach USD 54.47 billion by 2033, and this growth is primarily driven by the rising need for data-driven decision-making in the insurance sector. The same study also revealed that, as claims processes are becoming complex, challenges like rising fraud and the push for personal line products force the insurance companies to adopt data analytics and AI.

Profitability Got Harder: Loss costs are more volatile (catastrophe, repair, medical), so carriers need finer-grain insight to protect combined ratios.

Claims are Getting Automated: To do fast, straight-through claims, you need reliable data and models (fraud, severity, triage).

New Data Sources Arrived: Telematics, IoT, geospatial, third-party scores—more signals than most cores can handle today.

Regulators/Customers Want Transparency: Decisions must be explainable, which requires better data lineage and quality.

Biggest Roadblocks Stopping the Insurance Industry from Leveraging Data

Why do insurers fail to leverage their data? Despite heavy investment in data lakes and AI, many carriers struggle to turn data into underwriting lifts, faster claims, or lower combined ratios. The blockers include:

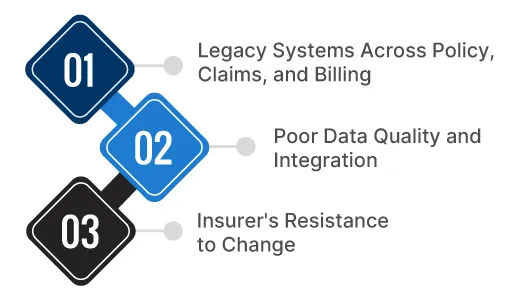

1. Legacy Systems Across Policy, Claims, and Billing

Core systems were built at different times and rarely talked to each other. Policy data sits apart from claims notes, billing history, and agent interactions, so analysts cannot form a single, trusted customer or risk view. This slows underwriting, weakens pricing accuracy, and makes claims analytics harder than they should be.

2. Poor Data Quality and Integration

Information saved on different sources is frequently not accurate, incomplete, or inconsistent. Data analysts put more time into searching, cleaning, and preparing data to be analyzed, as opposed to actual analysis. This lack of a “single source of truth” erodes belief in analytics and causes bad decisions.

3. Insurer’s Resistance to Change

The long history of the insurance industry has been to use intuition, experience, and manual methods to make decisions. Switching to a culture of basing decisions on data involves a big change in management and visionary leadership by top management, which may be subject to internal resistance.

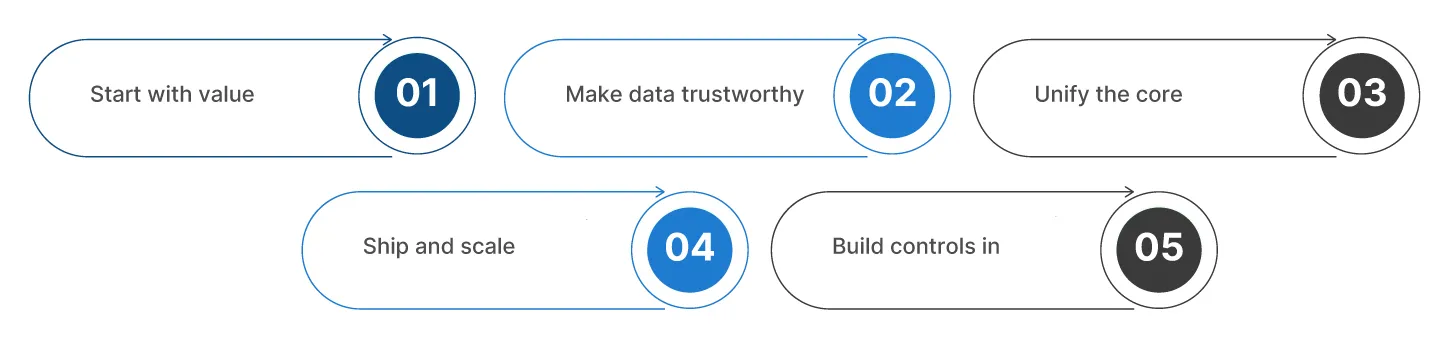

From Vision to Execution: A 5-Step Data Roadmap for Insurers

Here is a simple path for insurance enterprises to turn data into real business impact. The points below outline how this can be done and ensure that you make the best use of data.

Start with value: Choose three to five use cases that map to clear business outcomes such as loss ratio, FNOL time, fraud hit rate, and retention. Set a baseline, set a target, and ship work that moves those numbers.

Make data trustworthy: Agree on golden sources, capture lineage, and apply simple quality rules. Stand up a data catalog and stewardship, so underwriters and adjusters trust the figures behind pricing and claims.

Unify the core: Connect policy, claims, and billing through a cloud-ready platform with standard APIs. Bring in outside signals such as telematics, weather, and credit, so models see the full picture and scale across lines.

Ship and scale: Pair a business product owner with data scientists and engineers. Use MLOps to move models from pilot to production and into the tools used daily by underwriters, adjusters, and agents.

Build controls in: Embed explainability, privacy, and audit trails from day one, so pricing and claims automation are clear and in compliance without slowing deployment.

How Leading Insurers are Turning Data Challenges into Results

Insurers are managing data infrastructure and turning it into opportunities for growth and digital transformation. By embedding AI, Machine Learning, and predictive analytics into underwriting, pricing, and claims management, carriers are cutting FNOL times, enhancing fraud detection, sharpening risk selection, and lifting retention.

AllState

Allstate uses data science across the policy and claims lifecycle. By mining historical claims data, its models predict claim propensity and likely severity, flag anomalous patterns for SIU review, and surface fraud risks earlier. Analytics also scores churn risk and triggers personalized retention offers (e.g., coverage tweaks or discounts), improving customer retention and operational efficiency.

MetLife

MetLife’s data scientists embed predictive modeling across underwriting and claims to fight fraud and sharpen risk selection. Working on a global scale, they continuously refine risk and mortality models to price policies more precisely and manage capital and financial risk more effectively. The result is fairer rates for customers, stronger fraud defenses, and steadier portfolio performance.

Build a Data Advantage with TxMinds Insurance Data Management Solutions

As a leading partner for insurance digital management solutions, we start with business outcomes, aligning use cases to loss and expense ratio goals, and designing the target data platform and operating model to achieve them. Our teams possess domain expertise in underwriting, claims, billing, and distribution, with global delivery capabilities to meet regional compliance requirements.

We unify policy, claims, and billing data on cloud-ready platforms, embed AI and analytics into frontline decisions, and apply rigorous quality engineering to deliver reliably at scale. Recent engagements have spanned insurer modernization programs, industry events, and executive advisory services, all anchored in measurable business impact. Book a consultation with our industry experts to discover how we can help you bring real value through data analysis.

Rakesh Pal, Vice President at Tx and Head of Insurance Vertical, brings over 19+ years of experience in the insurance industry. His experience working with organizations like Cognizant, LTIMindtree, Valuemomentum, etc., brings him deep expertise in P&C (Re)Insurance across Personal, Commercial, and Specialty lines and its operational nuances across North America, Lloyd’s of London, Middle East, APAC, and India. With a strong background in digital transformation, cloud migration, domain advisory, and client delivery, he leads strategic initiatives that drive innovation, operational efficiency, and customer delight in the insurance industry. His leadership across delivery and solutions enables insurers to modernize their technology landscape and navigate evolving business, customer, and regulatory demands with confidence.

FAQs

What is the role of data in insurance?

Data powers accurate risk assessment, pricing, fraud detection, and claims decisions, helping insurers improve profitability and deliver more personalized, transparent products.

Why is data analytics now critical for insurers?

The insurance analytics market is projected to reach USD 54.47B by 2033, as carriers need data and AI to handle complex claims, rising fraud, new data sources (telematics, IoT), and demands for transparent, personalized products.

How can insurers start unlocking value from their data?

Begin with 3–5 high-impact use cases (e.g., loss ratio, FNOL time, fraud hit rate), improve data quality and integration, unify policy/claims/billing on a modern platform, and productionize AI models with governance and explainability built in.