Recommended Blogs

Blog

The Economics of Automation: Driving ROI in Insurance Transformation

Table of Content

- Insurance Economics Are Shifting: Why Efficiency Alone Isn’t Enough

- Where Intelligent Automation Unlocks P&L Gains Across the Value Chain

- A Practical ROI Framework for Insurance Leaders

- How TxMinds Enables Measurable Outcomes for Insurers

Share On

Insurance transformation is no longer a technological conversation; it’s an economic imperative. As insurers navigate rising customer expectations, expanding regulatory demands, and legacy systems that strain under modern workloads, automation has become the engine for powering digital growth. Yet, beyond the buzzwords and modernization promises lies a hard financial truth: automation delivers real ROI when executed with precision, scaled intelligently, and aligned to business outcomes, not just IT goals.

This operational drag directly translates into lost revenue, higher risk, and increased cost-to-serve. Automation, when strategically implemented, flips this equation, unlocks faster cycle times, reduces operational cost, and provides a superior customer experience.

What emerges is a multiplier effect: automation enhances efficiency, reduces errors, improves customer satisfaction, and fuels continuous innovation, all while compounding ROI year after year.

This blog unpacks how insurers can harness the true economic value of automation across underwriting, policy servicing, claims, data migration, QA, and customer experience. We will explore the frameworks, metrics, and real-world strategies that separate automation investments that merely “reduce effort” from those that transform operating models and create measurable, enterprise-wide impact.

Key Takeaways

- Automation is now an economic lever in insurance, targeting loss, expense, and combined ratios and not just “efficiency.”

- AI-powered claims automation cuts processing time by up to 70% and saves about $6.5B annually.

- A solid ROI model tracks baseline unit costs, cost–risk–growth impact, and full TCO (process, tech, change).

- Lasting value comes from treating automation as an operating-model shift, with clear ownership and experts refocused on judgment work.

Insurance Economics Are Shifting: Why Efficiency Alone Isn’t Enough

The economics of insurance are shifting in ways that traditional levers can no longer fully address. Rising claims of severity, inflation in repair and medical costs, intense regulatory scrutiny, and customers who expect simple, fast, transparent service are putting pressure on margins from all sides. At the same time, many insurers are dealing with ageing platforms, fragmented processes, and talent shortages in underwriting, claims, finance, and operations.

In this context, the core question for insurance enterprises is no longer “How do we trim operating expense?” but “How do we change the way work is done across the value chain?” Insurers need operating models that can scale without a matching rise in cost, protect against leakage, and free specialists from repetitive tasks so they can focus on judgment, relationships, and complex decisions. Automation becomes relevant here to redesign how underwriting, claims, policy servicing, and support functions run, so that financial performance, control, and CX can move in the same direction.

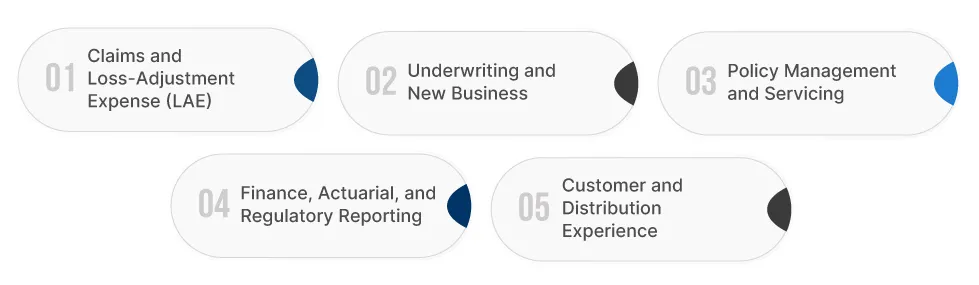

Where Intelligent Automation Unlocks P&L Gains Across the Value Chain

When applied with clear economic intent, intelligent automation in insurance becomes a direct lever on the loss ratio, expense ratio, and ultimately the combined ratio. Instead of isolated pilots, enterprises are now designing insurance workflow automation and intelligent process automation in insurance around specific value drivers. This is how automation drives ROI in insurance:

Claims and Loss-Adjustment Expense (LAE)

- Use case examples: Straight-through FNOL, automated validation of policy coverage, rules-based routing, and medical bill review.

- Economic Impact: AI-powered claims automation reduces processing time by up to 70% and saves an estimated $6.5 billion annually.

- Enablers: Combining rules, AI in insurance claims processing, and fraud detection automation in insurance to improve decision quality while keeping human oversight on complex cases.

Underwriting and New Business

- Use Case Examples: Pre-fill and validation of submission data, risk triage, automated referrals, and documentation checks.

- Economic Impact: Faster quote-to-bind, higher hit ratios, and better risk selection supported by automation for underwriting efficiency and real-time insurance analytics.

- Enablers: Targeted use of robotic process automation (RPA) in insurance to remove repetitive tasks so underwriters can focus on judgment and portfolio steering.

Policy Management and Servicing

- Use Case Examples: Automation for policy management across endorsements, renewals, cancellations, and billing adjustments.

- Economic Impact: Lower processing costs, fewer errors, improved compliance, and shorter cycle times for agents and customers.

- Enablers: End-to-end insurance workflow automation that connects front-office requests to back-office processing, with clear ownership of outcomes.

Finance, Actuarial, and Regulatory Reporting

- Use Case Examples: Automated reconciliations, data preparation for reserving and capital models, schedule production, and regulatory submissions.

- Economic Impact: Insurance automation cost savings reduced operational risk, and better use of scarce actuarial and finance expertise.

- Enablers: Repeatable process design combined with regulatory compliance automation to ensure consistency and auditability.

Customer and Distribution Experience

- Use Case Examples: Automated status updates on claims, self-service policy changes, real-time quotation, and straight-through onboarding for partners.

- Economic Impact: Improved NPS, higher retention, and increased agent productivity; core components of insurance automation ROI.

- Enablers: An insurance automation strategy that links front-end journeys with back-end processes, so customers and intermediaries feel the benefits of AI-driven insurance automation.

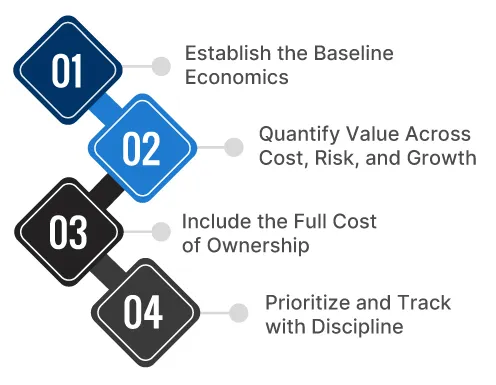

A Practical ROI Framework for Insurance Leaders

A strong insurance automation strategy starts with economics, not technology. The aim is to link insurance intelligent automation and intelligent process automation in insurance to metrics that matter:

1. Establish the Baseline Economics

Before any change, insurers need a clear view of current performance. That means understanding the cost per claim, cost per endorsement, average handling time, error rates, leakage sources, backlog levels, and how manual work affects service levels in underwriting, claims, and policy servicing.

2. Quantify Value Across Cost, Risk, and Growth

ROI from insurance automation should not be limited to headcount reduction.

- Cost: Fewer manual steps, less rework, lower vendor spending.

- Risk: Better fraud checks, stronger data quality, tighter compliance.

- Growth: Faster quote-to-bind, smoother policy management, better customer and partner experience.

Together, these elements create sustainable insurance automation of cost savings and revenue uplift.

3. Include the Full Cost of Ownership

To make insurance automation ROI credible, insurers must include process simplification, integration, licenses, support, and change management, including the effort to run and refine robotic process automation (RPA) in insurance and other automation assets. Clear ownership of both investment and benefits is essential.

4. Prioritize and Track with Discipline

Leading insurers treat intelligent automation use cases in insurance as a portfolio, ranking them by impacting P&L, complexity, and time to value. Early focus often goes to high-volume, rules-based activities in claims and servicing, while more advanced analytics and real-time insurance analytics follow once foundations are in place.

How TxMinds Enables Measurable Outcomes for Insurers

We help insurers turn automation from a concept into a measurable improvement in their P&L. We start by modernizing core platforms for policy, billing, claims, and underwriting, so workflow automation sits on secure, scalable systems rather than fragile legacy environments

On that foundation, we design and build insurance-specific automated journeys through underwriting, rating, and claims. We use accelerators for platforms like Guidewire, Duck Creek, and Majesco, along with intelligent test automation, DevSecOps, and quality engineering, to cut delivery risk and time to value. The result is not just new technology, but faster launches, lower run costs, and more reliable operations that sustain the business case for automation over time.

Rakesh Pal

VP, Insurance Vertical Head

Rakesh Pal, Vice President at Tx and Head of Insurance Vertical, brings over 19+ years of experience in the insurance industry. His experience working with organizations like Cognizant, LTIMindtree, Valuemomentum, etc., brings him deep expertise in P&C (Re)Insurance across Personal, Commercial, and Specialty lines and its operational nuances across North America, Lloyd’s of London, Middle East, APAC, and India. With a strong background in digital transformation, cloud migration, domain advisory, and client delivery, he leads strategic initiatives that drive innovation, operational efficiency, and customer delight in the insurance industry. His leadership across delivery and solutions enables insurers to modernize their technology landscape and navigate evolving business, customer, and regulatory demands with confidence.

FAQs

How does automation drive ROI in insurance?

Automation drives ROI in insurance by reducing manual effort and errors, lowering the cost per claim/endorsement, accelerating quote-to-bind and claims decisions, and enhancing retention and combined ratio over time.

What are the best practices for insurance automation and ROI?

Best practices for insurance automation and ROI include starting with baseline economics, prioritizing high-volume rule-based processes, treating use cases as a portfolio, and tying every initiative to clear cost, risk, and growth metrics.

What are the most impactful intelligent automation use cases in insurance?

High-impact intelligent automation use cases in insurance span straight-through FNOL, automated coverage validation, underwriting pre-fill and triage, policy servicing workflows, and finance/regulatory reporting automation.

How should insurers approach measuring the financial impact of insurance automation?

Measuring the financial impact of insurance automation means tracking changes in unit costs, leakage, cycle times, error rates, and retention against a pre-automation baseline.

Discover more