Recommended Blogs

Blog

Intelligent Underwriting: Moving Beyond Risk Assessment to Risk Advantage

Table of Content

- Why Intelligent Underwriting Is the Turning Point for Insurers

- How AI, Data, and Automation Transform the Underwriting Process?

- Real Business Benefits: From Speed to Strategic Risk Advantage

- Overcoming Modernization Challenges and Building the Future of Underwriting

Share On

The old ways of underwriting played a key role for many years. But in the current insurance landscape, they are falling short. Systems built on outdated data and rigid rules cannot match the pace of today’s market. With technology evolving rapidly, climate risks growing more complex, and customer needs shifting constantly, insurers must rethink how they approach risk.

Many policyholders already feel the strain. Around 42% of policyholders say the current process of getting a quotation is lengthy and complicated. That signals a clear need for change. Intelligent underwriting offers that change by moving from passive evaluation to active risk management. With the support of artificial intelligence, machine learning, and live data streams, insurers can build flexible risk profiles that adapt in real time.

It is not only about improving how risk is priced. It is about discovering new growth areas, improving portfolio performance, and giving customers the fast, personalized service they expect.

In this blog, you will explore how intelligent underwriting powered by AI and real-time data is reshaping the insurance sector. You will learn what works, what challenges to expect, and how forward-thinking insurers are using risk as a competitive edge.

Key Takeaways

- 42% of policyholders find the quoting process slow and complicated, showing the need for faster underwriting.

- AI and ML are already improving underwriting outcomes, according to 62% of executives.

- Automation accelerates decision-making and allows underwriters to focus on higher-value tasks.

- Intelligent underwriting enhances risk management, portfolio performance, and customer personalization.

Why Intelligent Underwriting Is the Turning Point for Insurers

For many years, underwriting depended on static models that used historical data and rule-based logic to evaluate risk. This approach worked well in more predictable times, but it is proving inadequate in today’s rapidly shifting environment.

Risks are now more complex and dynamic. Technological disruptions, climate volatility, and evolving customer expectations are changing the game. At the same time, policyholders want faster decisions and more personalized services. Insurers that rely on slow, manual underwriting processes are at risk of losing ground in both revenue and relevance.

Intelligent underwriting offers a new path forward. It moves beyond assessing past risk and focuses on managing it as a forward-looking asset. In fact, 62% of executives say that artificial intelligence and machine learning are already improving underwriting outcomes. These technologies help build adaptive risk models by analyzing real-time data and predicting future patterns.

This shift enables insurers to reduce price risk with greater accuracy, uncover risk management opportunities, and deliver stronger customer engagement. Intelligent underwriting is not just a tool for improvement; it is a foundation for competitive advantage in the future of insurance.

How AI, Data, and Automation Transform the Underwriting Process?

AI, ML, and automation are changing the way underwriting works in a big way. These technologies are more than simply tools; they are what make underwriting choices smarter, faster, and more accurate. Intelligent underwriting turns risk assessment from a human, time-consuming chore into a strategic advantage that drives growth and efficiency by unleashing the power of different data and automating complex activities.

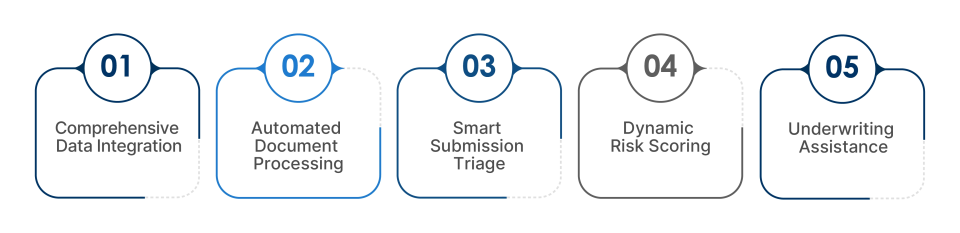

1. Comprehensive Data Integration

AI collects and analyzes a vast array of data, including demographic information, financial records, past claims, IoT sensor data, and social media activity, creating more robust and accurate risk profiles. Unlike traditional underwriting models that rely on limited and historical data, intelligent underwriting systems integrate real-time data across multiple touchpoints, providing a richer view of the evolving risk landscape for each applicant.

2. Automated Document Processing

Natural Language Processing (NLP) and Optical Character Recognition (OCR) are two technologies that make it possible to automatically extract and analyze data from unstructured documents like insurance applications, medical reports, and claims histories. This automation cuts down on the amount of work that needs to be done by hand and lessens the chance of making mistakes, speeding up the underwriting process and making it more accurate.

3. Smart Submission Triage

AI platforms assess incoming applications based on various factors, such as risk complexity, potential profitability, and alignment with the insurer’s risk appetite. Low-risk applications are automatically processed, allowing human underwriters to focus on more complex or high-risk cases that require expert judgment. This helps improve operational efficiency and reduces decision timelines.

4. Dynamic Risk Scoring

Machine learning models continuously update risk scores in response to real-time data inputs, allowing insurers to dynamically adjust pricing and coverage terms. This adaptability enables insurers to respond to emerging risks, optimize their portfolios, and offer competitive pricing tailored to each individual policyholder’s risk profile. For example, auto insurers are using telematics to adjust premiums in real time, health insurers are integrating wearable data to anticipate risks, and commercial carriers are leveraging climate models to underwrite catastrophe exposures more accurately

5. Underwriting Assistance

Intelligent virtual assistants manage routine tasks like requesting missing documents or explaining underwriting decisions, while notifying underwriters only when their expertise is needed. By automating administrative tasks, these virtual assistants empower underwriters to focus on more strategic, high-impact decisions that influence business outcomes.

Real Business Benefits: From Speed to Strategic Risk Advantage

Intelligent underwriting offers clear, measurable advantages that directly impact business performance and growth. It goes beyond speeding up workflows by helping insurers make smarter decisions, improve customer experience, and manage risk effectively across portfolios.

- Accelerated Decision-Making: With AI-driven tools, underwriting timelines are shortened dramatically. What once took days or even weeks can now be completed in hours or minutes. This boosts efficiency while giving customers faster, smoother experience.

- Increased Accuracy and Reduced Risk: Machine learning reveals patterns that traditional models might miss. This leads to more accurate pricing, fewer underwriting mistakes, and a reduced chance of underwriting leakage.

- Operational Efficiency and Cost Savings: By automating routine steps, underwriters can shift focus to higher-value tasks. This not only raises team productivity but also helps reduce the time and resources spent on manual processes.

- Enhanced Customer Personalization: With access to real-time data, insurers can adjust policies and pricing to match individual customer needs. This tailored approach improves satisfaction and strengthens long-term relationships.

- Improved Risk Portfolio Management: Insurers gain better visibility into where the real opportunities and risks lie. This helps them adjust strategies in advance and make well-informed decisions that lead to stronger portfolio health and retention.

- Stronger Compliance and Transparency: AI systems ensure underwriting rules are applied consistently. They also generate clear audit trails, making it easier to meet regulatory requirements and demonstrate good governance.

Overcoming Modernization Challenges and Building the Future of Underwriting

While intelligent underwriting holds immense promises, insurers face a series of complex challenges that can slow down or complicate adoption. Fragmented data ecosystems, manual-heavy processes, and cultural resistance often undermine efficiency and delay transformation. In addition, increasing regulatory scrutiny and integration complexities demand a holistic approach—one that combines technology modernization, workforce readiness, and strong governance frameworks.

Key Challenges Insurers Must Address:

- Data Fragmentation and Quality: Insurers often grapple with inconsistent, incomplete, or siloed data, which reduces the accuracy of AI-driven insights and weakens decision-making confidence. Unlocking value requires strong data governance, harmonization, and enrichment strategies.

- Manual Processes: Legacy underwriting still relies heavily on manual data entry and document handling, creating bottlenecks and inefficiencies. Modernization requires investment in automation, workflow orchestration, and continuous upskilling of underwriters to work alongside intelligent tools.

- Cultural and Organizational Resistance: Adoption hurdles often stem from fear of job displacement or mistrust of AI. Overcoming this requires proactive change management, transparent communication, and demonstrating how AI augments rather than replaces underwriting expertise.

- Regulatory Compliance and Transparency: As AI becomes embedded in underwriting, insurers must ensure fairness, explainability, and auditability of decisions. Global regulators are raising the bar with frameworks such as the NAIC AI Principles (U.S.) and the EU AI Act. Insurers must balance innovation with ethical AI, bias mitigation, and regulatory trustworthiness.

- System Integration Complexity: Introducing AI into legacy underwriting platforms is rarely seamless. Success demands careful planning, phased execution, and scalable architecture to avoid operational disruptions.

At TxMinds, we understand these challenges deeply and offer end-to-end intelligent underwriting solutions that combine the latest AI and automation technologies with expert change management. Our approach ensures seamless integration, strong data governance, and underwriter empowerment to help insurers unlock underwriting agility, precision, and strategic risk advantage in a compliant and transparent manner.

Connect with TxMinds to take the next step toward modernizing your underwriting capabilities with confidence.

Rakesh Pal

VP, Insurance Vertical Head

Rakesh Pal, Vice President at Tx and Head of Insurance Vertical, brings over 19+ years of experience in the insurance industry. His experience working with organizations like Cognizant, LTIMindtree, Valuemomentum, etc., brings him deep expertise in P&C (Re)Insurance across Personal, Commercial, and Specialty lines and its operational nuances across North America, Lloyd’s of London, Middle East, APAC, and India. With a strong background in digital transformation, cloud migration, domain advisory, and client delivery, he leads strategic initiatives that drive innovation, operational efficiency, and customer delight in the insurance industry. His leadership across delivery and solutions enables insurers to modernize their technology landscape and navigate evolving business, customer, and regulatory demands with confidence.

FAQs

What is intelligent underwriting?

Intelligent underwriting uses AI, ML, and real-time data to create adaptive risk profiles, enabling insurers to make faster, more accurate, and strategic risk decisions.

How does AI improve the underwriting process?

AI integrates diverse data sources, automates document processing, triages submissions, and dynamically updates risk scores to speed up decision-making and reduce errors.

What are the main benefits of intelligent underwriting?

It improves efficiency, accuracy, and customer personalization while enhancing portfolio management, compliance, and overall strategic advantage for insurers.

What challenges do insurers face when implementing intelligent underwriting?

Insurers may encounter fragmented data, legacy manual processes, cultural resistance, regulatory compliance requirements, and system integration complexities that require careful planning and change management.

Discover more